All Categories

Featured

Table of Contents

The are entire life insurance coverage and universal life insurance coverage. The money value is not included to the death benefit.

The policy finance rate of interest rate is 6%. Going this path, the passion he pays goes back into his policy's cash money worth instead of an economic establishment.

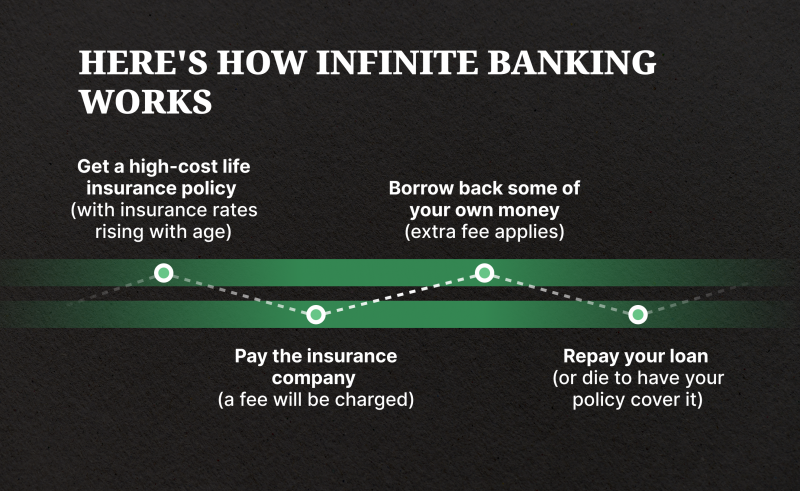

Imagine never ever needing to stress over small business loan or high rate of interest once again. What if you could obtain money on your terms and build riches concurrently? That's the power of boundless banking life insurance coverage. By leveraging the money value of whole life insurance policy IUL policies, you can expand your wealth and borrow cash without depending on conventional financial institutions.

There's no set car loan term, and you have the liberty to choose the repayment schedule, which can be as leisurely as paying back the loan at the time of death. This versatility encompasses the servicing of the fundings, where you can decide for interest-only payments, maintaining the finance equilibrium flat and workable.

Holding money in an IUL dealt with account being credited rate of interest can typically be far better than holding the cash money on deposit at a bank.: You have actually always fantasized of opening your own bakery. You can obtain from your IUL policy to cover the initial costs of leasing a space, buying devices, and hiring personnel.

Direct Recognition Whole Life

Individual loans can be obtained from traditional financial institutions and debt unions. Below are some bottom lines to consider. Credit score cards can offer a versatile method to obtain cash for very short-term periods. Borrowing money on a debt card is usually really expensive with annual percentage rates of passion (APR) commonly reaching 20% to 30% or more a year.

The tax treatment of policy fundings can differ considerably depending upon your country of residence and the particular terms of your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are generally tax-free, offering a considerable benefit. In other jurisdictions, there might be tax ramifications to think about, such as prospective tax obligations on the loan.

Term life insurance coverage only supplies a fatality benefit, without any kind of cash worth buildup. This implies there's no cash money worth to borrow against.

Infinite Financial Systems

When you initially hear concerning the Infinite Financial Principle (IBC), your initial response could be: This seems as well excellent to be true. The trouble with the Infinite Financial Idea is not the idea yet those individuals providing an unfavorable review of Infinite Banking as a principle.

So as IBC Authorized Practitioners via the Nelson Nash Institute, we assumed we would certainly respond to several of the top inquiries people look for online when discovering and understanding whatever to do with the Infinite Financial Concept. What is Infinite Banking? Infinite Financial was produced by Nelson Nash in 2000 and fully discussed with the magazine of his publication Becoming Your Own Lender: Open the Infinite Financial Concept.

Infinite Banking Uk

You assume you are coming out economically ahead since you pay no passion, however you are not. With conserving and paying money, you may not pay passion, but you are using your money once; when you spend it, it's gone permanently, and you offer up on the possibility to make life time substance rate of interest on that money.

Also banks use entire life insurance coverage for the same objectives. The Canada Earnings Agency (CRA) even acknowledges the value of getting involved entire life insurance coverage as a special property course utilized to create long-lasting equity safely and naturally and give tax obligation advantages outside the range of standard financial investments.

Ibc Infinite Banking Concept

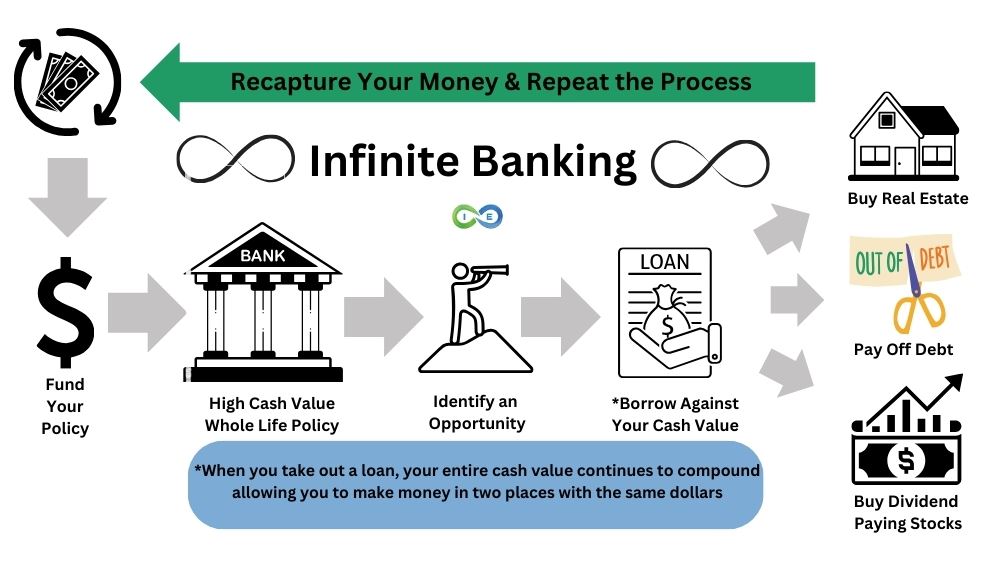

It permits you to create wealth by satisfying the financial function in your very own life and the ability to self-finance major way of life acquisitions and expenditures without interrupting the compound interest. One of the easiest ways to think of an IBC-type getting involved entire life insurance policy is it approaches paying a mortgage on a home.

When you obtain from your taking part whole life insurance coverage plan, the cash money worth continues to expand nonstop as if you never borrowed from it in the very first place. This is since you are using the cash money worth and death advantage as security for a loan from the life insurance policy firm or as collateral from a third-party lending institution (understood as collateral borrowing).

That's why it's vital to deal with a Licensed Life insurance policy Broker licensed in Infinite Financial who structures your taking part entire life insurance coverage policy correctly so you can stay clear of adverse tax obligation implications. Infinite Banking as a monetary method is except everyone. Right here are a few of the advantages and disadvantages of Infinite Banking you should seriously take into consideration in deciding whether to relocate forward.

Our recommended insurance coverage provider, Equitable Life of Canada, a shared life insurance firm, focuses on getting involved whole life insurance policy policies particular to Infinite Financial. Also, in a common life insurance policy firm, insurance holders are taken into consideration firm co-owners and receive a share of the divisible surplus generated yearly with returns. We have a variety of service providers to choose from, such as Canada Life, Manulife and Sunlight Lifedepending on the requirements of our clients.

Please additionally download our 5 Top Concerns to Ask An Infinite Banking Agent Before You Work with Them. For more details concerning Infinite Financial go to: Disclaimer: The product provided in this newsletter is for informational and/or academic objectives just. The information, point of views and/or sights shared in this newsletter are those of the writers and not necessarily those of the distributor.

Infinite Banking Insurance Policy

The principle of Infinite Banking was produced by Nelson Nash in the 1980s. Nash was a financing professional and follower of the Austrian college of economics, which promotes that the worth of items aren't clearly the result of traditional economic structures like supply and demand. Instead, individuals value money and items in a different way based on their financial standing and demands.

One of the risks of conventional banking, according to Nash, was high-interest prices on financings. Too many individuals, himself consisted of, got right into economic problem due to reliance on banking establishments.

Infinite Financial requires you to own your monetary future. For goal-oriented people, it can be the best monetary tool ever. Here are the advantages of Infinite Banking: Arguably the single most useful aspect of Infinite Banking is that it boosts your cash money circulation.

Dividend-paying whole life insurance policy is really low danger and offers you, the insurance policy holder, a lot of control. The control that Infinite Banking uses can best be organized into 2 groups: tax benefits and asset securities. One of the reasons entire life insurance coverage is suitable for Infinite Banking is exactly how it's tired.

Entire life insurance policy plans are non-correlated assets. This is why they function so well as the economic structure of Infinite Banking. Despite what occurs in the marketplace (stock, property, or otherwise), your insurance plan maintains its worth. A lot of individuals are missing out on this important volatility barrier that helps protect and expand riches, rather breaking their money into 2 buckets: savings account and investments.

Market-based investments expand wealth much faster yet are revealed to market variations, making them naturally risky. What if there were a third pail that offered safety and security but likewise moderate, surefire returns? Whole life insurance policy is that third pail. Not just is the rate of return on your entire life insurance policy assured, your death benefit and costs are additionally ensured.

What Is Infinite Banking Concept

Infinite Financial allures to those looking for higher monetary control. Tax obligation effectiveness: The money value expands tax-deferred, and policy loans are tax-free, making it a tax-efficient tool for developing riches.

Property protection: In numerous states, the cash value of life insurance policy is shielded from creditors, including an extra layer of monetary safety. While Infinite Banking has its qualities, it isn't a one-size-fits-all option, and it features significant downsides. Here's why it might not be the very best strategy: Infinite Banking frequently calls for complex policy structuring, which can puzzle policyholders.

{kind=link}

Latest Posts

Bank On Yourself Life Insurance

How To Be Your Own Bank - Simply Explained - Chris Naugle

Becoming Your Own Banker